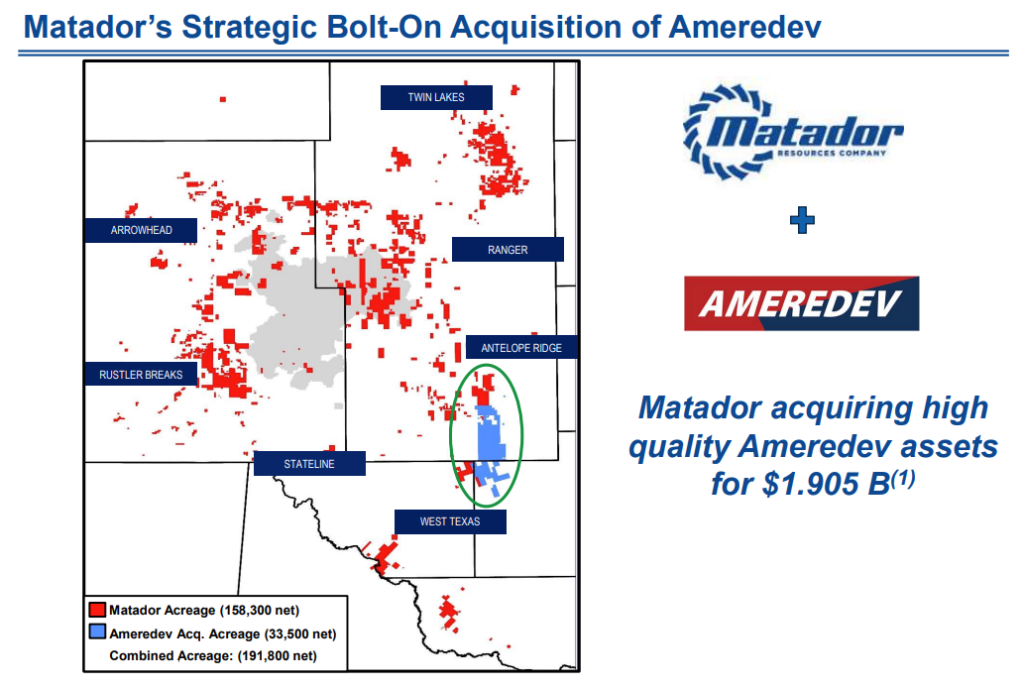

DALLAS–(BUSINESS WIRE)–Jun. 12, 2024– Matador Resources Company (NYSE: MTDR) (“Matador” or the “Company”) today announced that a wholly-owned subsidiary of Matador has entered into a definitive agreement to acquire a subsidiary of Ameredev II Parent, LLC (“Ameredev”), including certain oil and natural gas producing properties and undeveloped acreage located in Lea County, New Mexico and Loving and Winkler Counties, Texas (the “Ameredev Acquisition”). The Ameredev Acquisition also includes an approximate 19% stake in Piñon Midstream, LLC (“Piñon”), which has midstream assets in southern Lea County, New Mexico. The consideration for the Ameredev Acquisition will consist of a cash payment of $1.905 billion, subject to customary closing adjustments. Ameredev is a portfolio company of EnCap Investments L.P. (“EnCap”).

The Ameredev Acquisition is subject to customary closing conditions and is expected to close late in the third quarter of 2024 with an effective date of June 1, 2024. A short slide presentation summarizing the Ameredev Acquisition is also included on the Company’s website at www.matadorresources.com on the Events and Presentations page under the Investor Relations tab. Matador’s management will host a live conference call to discuss the Ameredev Acquisition on Wednesday, June 12, 2024 at 10:00 am Central Time. Further details are provided at the end of this press release.

Joseph Wm. Foran, Matador’s Founder, Chairman and CEO, commented, “Matador is very excited to work with EnCap again on this strategic bolt-on opportunity (see Exhibit A). As with the successful Advance Energy deal we completed in April of 2023, we view the Ameredev transaction as another unique opportunity to work with EnCap and another value-creating opportunity for Matador and its shareholders. We evaluated this opportunity based on the high rock quality, the strong existing production and cash flow profile, the significant reserves additions, the high-quality inventory, the strategic fit within our existing portfolio of properties and the expansion of our midstream footprint with an ownership interest in Piñon. The equity and debt securities offerings and the revolving credit facility amendment we completed earlier this year, together with our historical balance sheet conservatism, have provided Matador with the opportunity to acquire these high-quality assets and continue Matador’s consistent history of profitable growth at a measured pace.”

via June 2024 Annual Shareholders Meeting Presentation

Transaction Highlights

- On a pro forma basis following closing of the acquisition, Matador expects to have over 190,000 net acres in the Delaware Basin, approximately 2,000 net locations, production of over 180,000 barrels of oil and natural gas equivalent (“BOE”) per day, proved oil and natural gas reserves of over 580 million BOE and an enterprise value in excess of $10 billion (see Exhibit B)

- Expected to generate forward one-year Adjusted EBITDA1 of approximately $425 to $475 million at strip prices as of late May 2024, which represents an attractive purchase price multiple of 4.2x for the upstream assets:

- Strip prices for the remainder of 2024 averaged $77 per barrel of oil and $2.76 per MMBtu of natural gas.

- Accretive to relevant key financial and valuation metrics

- Significant increase in high quality pro forma drilling locations in primary development zones (see Exhibit C)

- PV-10 (present value discounted at 10%)2 at May 31, 2024 of $1.46 billion on total proved oil and natural gas reserves utilizing strip pricing as of late May 2024. The PV-10 of $1.46 billion does not include the interest in Piñon or certain undeveloped but prospective locations included in Matador’s valuation of the Ameredev assets:

- PV-10 of proved developed (PD) oil and natural gas reserves at May 31, 2024 of $1.20 billion, or approximately $47,100 per flowing BOE, utilizing strip pricing as of late May 2024.

- Preserves Matador’s strong balance sheet with pro forma leverage expected to be approximately 1.3x at closing and back below 1.0x by the middle of 2025 based upon current commodity prices, allowing Matador to maintain operational and financial flexibility while continuing to return value to shareholders through its fixed quarterly dividend and protecting cash flows through its appropriate commodity hedges

- Expanding Matador’s midstream footprint with an approximate 19% stake in Piñon, which allows for increased coordination between Matador and Piñon in gathering, transporting and treating natural gas from the Ameredev properties

Ameredev Asset Highlights

- Estimated production in the third quarter of 2024 of 25,000 to 26,000 BOE per day (65% oil)

- Approximately 33,500 highly contiguous net acres (82% held by production; over 99% operated) in the northern Delaware Basin, most of which is located in Matador’s Antelope Ridge asset area in southern Lea County, New Mexico and Matador’s West Texas asset area in Loving and Winkler Counties, Texas (see Exhibit A again)

- Adds 431 gross (371 net) operated locations (86% working interest) identified for future drilling, including prospective targets throughout the Wolfcamp and Bone Spring formations

- Locations are consistent with Matador’s methodology for estimating inventory with typically three to four (or fewer) locations per section, or the equivalent of 160-acre (or greater) spacing, in all prospective completion intervals

- Prior to transaction closing, Matador expects Ameredev to operate one drilling rig and to continue operations on 13 drilled but uncompleted (DUC) wells with one completion crew:

- The prospectivity of the Ameredev acreage immediately competes for development capital with Matador’s existing acreage (see Exhibit C again), so Matador expects to continue operating a total of nine drilling rigs for the immediate future on the combined approximately 192,000 net acres of the Matador-Ameredev properties.

- The additional ninth drilling rig and the associated Ameredev activities are not expected to increase the range of Matador’s estimated drilling, completing and equipping (“D/C/E”) capital expenditures of $1.10 to $1.30 billion for 2024. More information regarding the capital expenditures associated with the Ameredev Acquisition and its impact on Matador’s guidance for 2024 will be included in Matador’s press release announcing its second quarter 2024 results, which is expected to be issued in late July 2024.

Matador estimates total proved oil and natural gas reserves associated with the Ameredev properties of 118 million BOE (60% oil) at May 31, 2024. The pro forma combined company is estimated to have 578 million BOE, a 26% increase from Matador’s total proved reserves at December 31, 2023 of 460 million BOE (see Exhibit D). PV-10 of the proved oil and natural gas reserves of the Ameredev properties at May 31, 2024 was approximately $1.66 billion using the same unweighted arithmetic average first-day-of-the-month price methodology for the previous 12-month period being used to value the Company’s reserves, which are $74.91 per barrel of oil and $2.35 per MMBtu of natural gas. The PV-10 of $1.66 billion does not include the interest in Piñon or certain undeveloped but prospective locations included in Matador’s valuation of the Ameredev assets. Matador expects to add future proved reserves and reserves value as a result of the development of the Ameredev properties going forward. These reserves estimates were prepared by Matador’s engineering staff and audited by Netherland, Sewell & Associates, Inc., independent reservoir engineers, as of May 31, 2024.

Mr. Foran further commented, “We took significant strides during and shortly after the first quarter of 2024 to strengthen our balance sheet and allow us to participate in another special opportunity like this one. The specific location and quality of the Ameredev assets, the strong existing cash flow, the multi-pay potential and the cost savings associated with developing these assets via longer laterals on multi-well pads on blocky acreage were key features that attracted us to this unique opportunity and significantly enhance our already strong Delaware Basin portfolio and prospect inventory. This acquisition also positions Matador for continued success and growth throughout 2024, 2025 and into the future as one of the top ten producers in the Delaware Basin (see Exhibit E).

“To assist in financing this all-cash transaction, Matador has received firm commitments from PNC Bank, the lead bank under our reserves-based credit facility, to provide at closing (i) a 50% increase in the elected commitment under our credit facility from $1.5 billion to $2.25 billion and (ii) a $250 million Term Loan A under our credit facility to provide additional liquidity following the closing of the transaction. Importantly, this acquisition should not significantly impact Matador’s leverage profile in the long-term, as we expect our pro forma leverage ratio to return to a ratio below 1.0x by the middle of 2025 based upon current commodity prices. We especially appreciate PNC Bank for their leadership and support in arranging this financing commitment and the confidence and support we have received from the other members of our bank group.

“This transaction marks the second significant deal Matador has done with EnCap in the last 18 months. Gary Petersen, one of EnCap’s Founders, and I have known each other for many years. Similar to the Advance Energy transaction we closed in April of 2023, the long relationship with Gary and EnCap was critical to the smooth negotiation of this transaction. Thank you to Gary, the other senior members of the EnCap team, Parker Reese and the rest of the Ameredev team and the Matador team for their hard work and integrity in efficiently reaching a deal that we believe is a positive development for all parties. We also appreciate the support of our other friends, shareholders, bankers and vendors in making this deal happen. We look forward to the additional commercial opportunities and free cash flow that this new acreage and production will provide for Matador.”

Conference Call Information

Management will host a live conference call to discuss the Ameredev Acquisition on Wednesday, June 12, 2024 at 10:00 am Central Time. To access the live conference call by phone, you can use the following link https://register.vevent.com/register/BI43dafc62d9a54c13a8b9fab5e226a923 and you will be provided with dial-in details after registering. To avoid delays, it is recommended that participants dial into the conference call at least 15 minutes ahead of the scheduled start time.

The live conference call will also be available through the Company’s website at www.matadorresources.com on the Events and Presentations page under the Investor Relations tab. The replay for the event will be available on the Company’s website at www.matadorresources.com on the Events and Presentations page under the Investor Relations tab for one year following the date of the conference call.

Advisors

Baker Botts LLP served as legal advisor to Matador for the transaction. Vinson & Elkins LLP served as legal advisor and JP Morgan served as financial advisor to Ameredev and EnCap.

About Matador Resources Company

Matador is an independent energy company engaged in the exploration, development, production and acquisition of oil and natural gas resources in the United States, with an emphasis on oil and natural gas shale and other unconventional plays. Its current operations are focused primarily on the oil and liquids-rich portion of the Wolfcamp and Bone Spring plays in the Delaware Basin in Southeast New Mexico and West Texas. Matador also operates in the Eagle Ford shale play in South Texas and the Haynesville shale and Cotton Valley plays in Northwest Louisiana. Additionally, Matador conducts midstream operations in support of its exploration, development and production operations and provides natural gas processing, oil transportation services, oil, natural gas and produced water gathering services and produced water disposal services to third parties.

For more information, visit Matador Resources Company at www.matadorresources.com.

Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. “Forward-looking statements” are statements related to future, not past, events. Forward-looking statements are based on current expectations and include any statement that does not directly relate to a current or historical fact. In this context, forward-looking statements often address expected future business and financial performance, and often contain words such as “could,” “believe,” “would,” “anticipate,” “intend,” “estimate,” “expect,” “may,” “should,” “continue,” “plan,” “predict,” “potential,” “project,” “hypothetical,” “forecasted” and similar expressions that are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. Such forward-looking statements include, but are not limited to, statements about the consummation and timing of the Ameredev Acquisition, the anticipated benefits, opportunities and results with respect to the acquisition, including the expected value creation, reserves additions, midstream opportunities and other anticipated impacts from the Ameredev Acquisition, as well as other aspects of the transaction, guidance, projected or forecasted financial and operating results, future liquidity, the payment of dividends, results in certain basins, objectives, project timing, expectations and intentions, regulatory and governmental actions and other statements that are not historical facts. Actual results and future events could differ materially from those anticipated in such statements, and such forward-looking statements may not prove to be accurate. These forward-looking statements involve certain risks and uncertainties, including, but not limited to, the ability of the parties to consummate the Ameredev Acquisition in the anticipated timeframe or at all; risks related to the satisfaction or waiver of the conditions to closing the Ameredev Acquisition in the anticipated timeframe or at all; risks related to obtaining the requisite regulatory approvals; disruption from the Ameredev Acquisition making it more difficult to maintain business and operational relationships; significant transaction costs associated with the Ameredev Acquisition; the risk of litigation and/or regulatory actions related to the Ameredev Acquisition, as well as the following risks related to financial and operational performance: general economic conditions; the Company’s ability to execute its business plan, including whether its drilling program is successful; changes in oil, natural gas and natural gas liquids prices and the demand for oil, natural gas and natural gas liquids; its ability to replace reserves and efficiently develop current reserves; the operating results of the Company’s midstream oil, natural gas and water gathering and transportation systems, pipelines and facilities, the acquiring of third-party business and the drilling of any additional salt water disposal wells; costs of operations; delays and other difficulties related to producing oil, natural gas and natural gas liquids; delays and other difficulties related to regulatory and governmental approvals and restrictions; impact on the Company’s operations due to seismic events; its ability to make acquisitions on economically acceptable terms; its ability to integrate acquisitions; disruption from the Company’s acquisitions making it more difficult to maintain business and operational relationships; significant transaction costs associated with the Company’s acquisitions; the risk of litigation and/or regulatory actions related to the Company’s acquisitions; availability of sufficient capital to execute its business plan, including from future cash flows, available borrowing capacity under its revolving credit facilities and otherwise; the operating results of and the availability of any potential distributions from our joint ventures; weather and environmental conditions; and the other factors that could cause actual results to differ materially from those anticipated or implied in the forward-looking statements. For further discussions of risks and uncertainties, you should refer to Matador’s filings with the Securities and Exchange Commission (“SEC”), including the “Risk Factors” section of Matador’s most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q. Matador undertakes no obligation to update these forward-looking statements to reflect events or circumstances occurring after the date of this press release, except as required by law, including the securities laws of the United States and the rules and regulations of the SEC. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. All forward-looking statements are qualified in their entirety by this cautionary statement.

1 Adjusted EBITDA is a non-GAAP financial measure. The Company defines Adjusted EBITDA as earnings before interest expense, income taxes, depletion, depreciation and amortization, accretion of asset retirement obligations, property impairments, unrealized derivative gains and losses, certain other non-cash items and non-cash stock-based compensation expense and net gain or loss on asset sales and impairment. The most comparable GAAP measures to Adjusted EBITDA are net income or net cash provided by operating activities. The Company has not provided such GAAP measures or a reconciliation to such GAAP measures because they would be preliminary and prospective in nature and would not be able to be prepared without estimation of a number of variables that are unknown at this time.

2 PV-10 is a non-GAAP financial measure, which differs from the GAAP financial measure of “Standardized Measure” because PV-10 does not include the effects of income taxes on future income. The income taxes related to the acquired properties is unknown at this time because the Company’s tax basis in such properties will not be known until the closing of the transaction and is subject to many variables. As such, the Company has not provided the Standardized Measure of the acquired properties or a reconciliation of PV-10 to Standardized Measure.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240612279533/en/

Mac Schmitz

Senior Vice President – Investor Relations

(972) 371-5225

investors@matadorresources.com

Source: Matador Resources Company